Investing

Record Profits, Rising Risks: What Bank Earnings Reveal About the Economy

Last Monday morning, Jamie Dimon walked into JPMorgan Chase headquarters on Park Avenue and delivered two pieces of news that shook Wall Street simultaneously: a record-shattering quarter and his own retirement timeline.

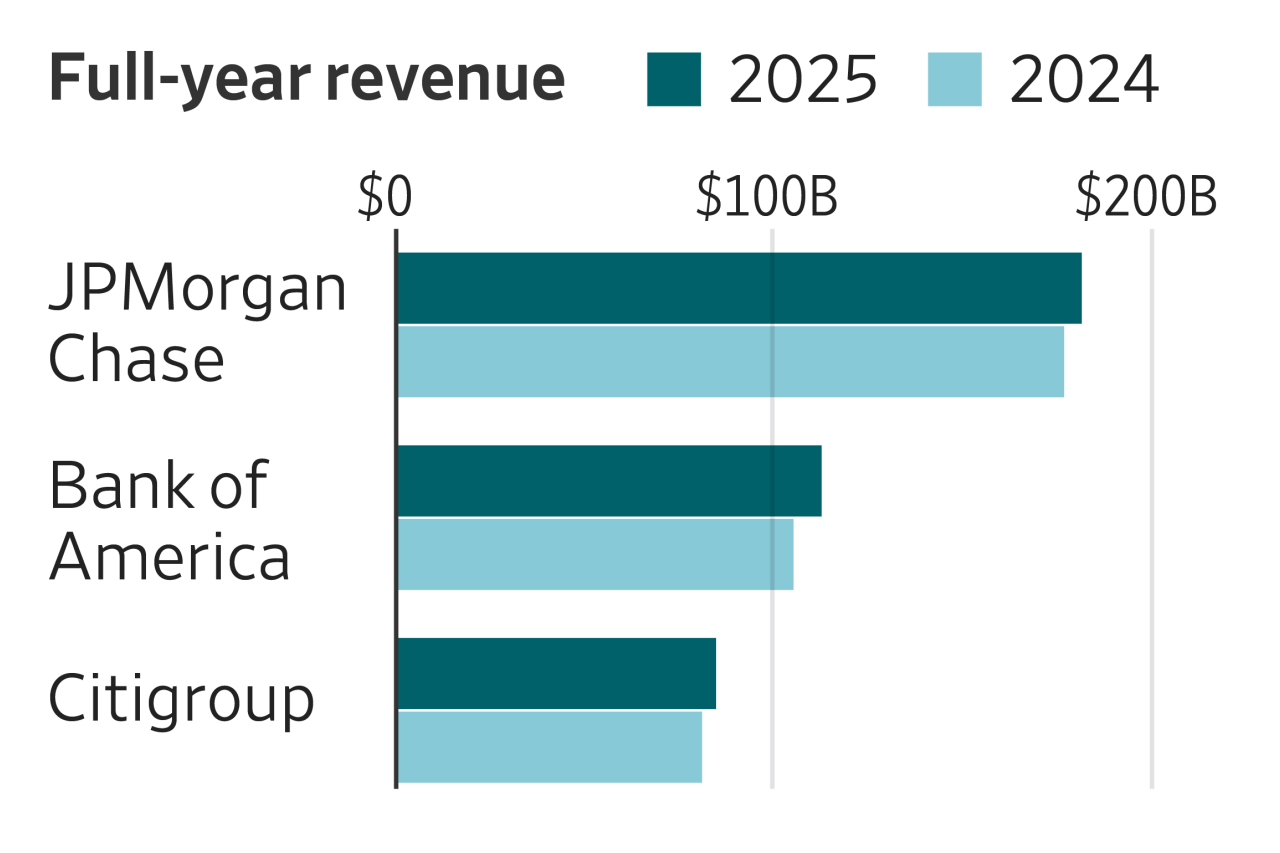

The numbers were remarkable. JPMorgan posted Q1 2026 net income of $16.4 billion, earnings per share of $5.42 -- comfortably beating the consensus estimate of $5.15 -- and total revenue of $49.2 billion, up 8% year-over-year. Shares surged 4.2% on the open to an all-time high of $248.50.

But here is the thing about record bank earnings in a volatile market: they are not just a story about one bank. They are a signal. A signal about where the economy actually stands, what is working, what is breaking, and -- most importantly for you as an investor -- where opportunity may be hiding underneath all the noise.

Because right now, there is a lot of noise.

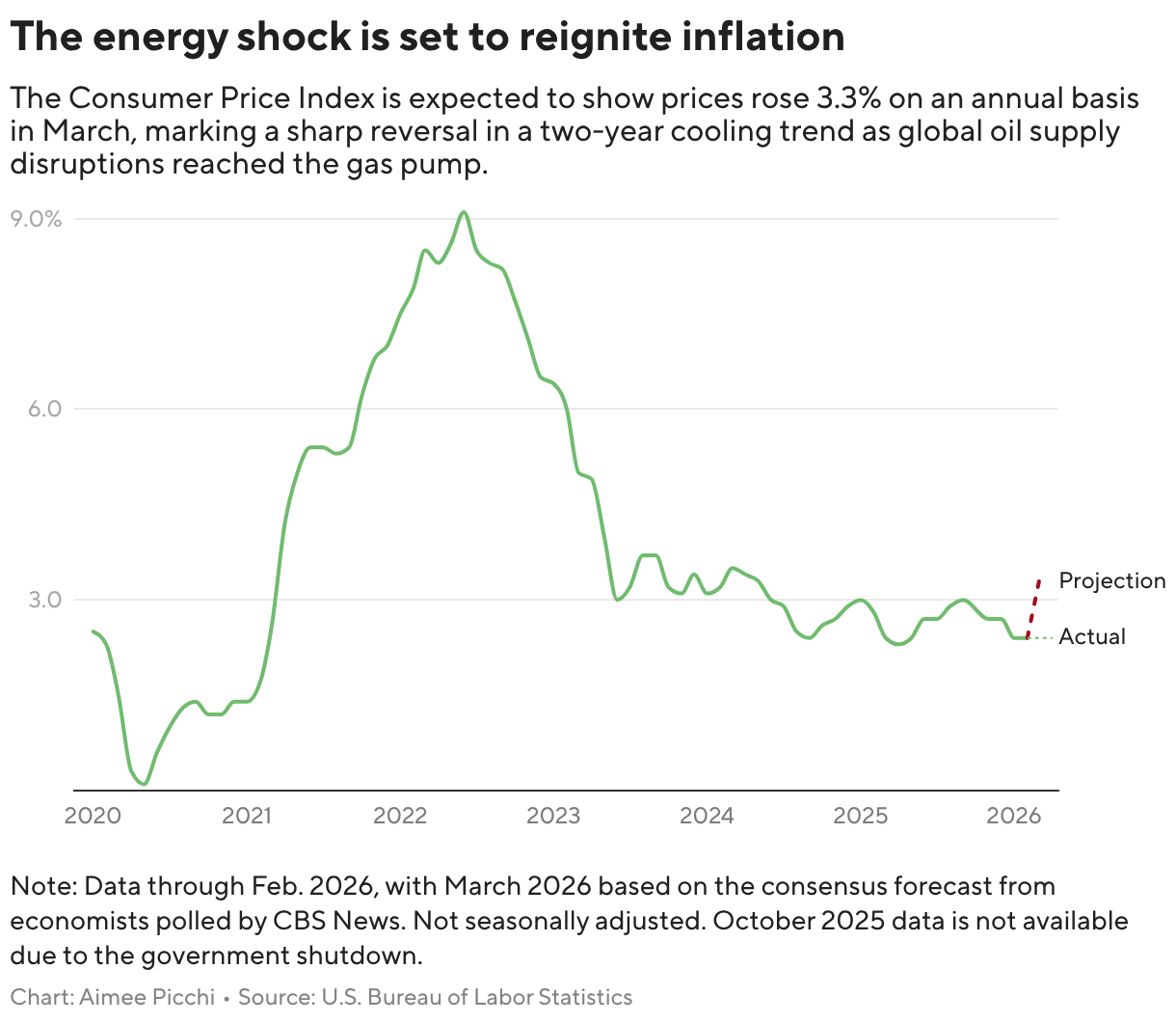

Oil is trading at $100-$113 a barrel. The S&P 500 is down nearly 4% for the year and struggling to hold above its 200-day moving average. Recession odds from Moody's have climbed to 49%. CPI hit 3.3% in March -- the highest since April 2024. The US-Iran conflict continues to rattle global shipping routes, with the Strait of Hormuz only partially reopened.

And yet: the world's largest bank just posted its best quarter ever.

What is really going on -- and what should you do about it?

The Dimon Legacy: What Record Profits Signal About the Economy

Banks are the circulatory system of any economy. When they earn record profits, it tells you the blood is still flowing -- loans are being made, businesses are borrowing, consumers are spending. When they start losing money, it is usually a leading indicator that the real economy is in trouble.

JPMorgan's Q1 2026 results revealed several important things about the current state of the economy:

- Consumers are still spending. Internal Chase card data showed discretionary spending up 2.6% year-to-date. People are still shopping, dining out, and booking travel -- even with $4+ gas prices. This is not a broken consumer. Yet.

- Investment banking is booming. Fees from M&A and IPO deals surged by mid-to-high teens year-over-year, fueled by a backlog of deals that were shelved during late-2025 volatility. Companies are merging. Capital is moving.

- Credit is normalizing, not collapsing. Net charge-offs (loans written off as bad debt) rose to about 3.4%, which sounds worrying until you compare it to the 5-6% levels seen during the 2008 crisis. This is not a credit crisis. It is a normalization.

- Net interest income remains massive. With the Fed holding rates at 3.5-3.75%, banks continue to earn the spread between what they pay depositors and what they charge on loans. JPMorgan guided for $104.5 billion in full-year 2026 NII.

Dimon himself struck a cautious note in his shareholder letter, warning that the Iran war "could reignite inflation and push recession odds meaningfully higher." But his bank's results tell a different story: the underlying economy is more resilient than the headlines suggest.

The Inflation Problem That Will Not Go Away

Here is the problem that JPMorgan's record profits cannot solve: inflation is rising again, and the Federal Reserve cannot do much about it.

March CPI came in at 3.3% year-over-year -- a significant jump from the 2.4% reading in January. The culprit is oil. With the Strait of Hormuz only partially accessible since the US-Iran conflict began in late February, energy prices have surged. West Texas Intermediate crude is trading between $100-$113 per barrel. US gasoline has crossed $4 per gallon nationally.

The problem with oil-driven inflation is structural: the Federal Reserve cannot fight it by raising rates. You cannot make oil cheaper by restricting credit. All the Fed can do is hold rates steady and hope the conflict resolves.

That is exactly what they are doing. At their March meeting, the FOMC held rates at 3.5-3.75% for the second consecutive meeting. The so-called "dot plot" still projects a single rate cut in 2026, but the timing has been pushed out. Seven of nineteen committee members now see no cuts at all this year. The 10-year Treasury yield is holding near 4.33%.

For investors, this creates a challenging environment:

- High rates compress valuations for growth stocks, especially high-PE tech companies

- Energy companies benefit directly from higher oil prices

- Utilities and consumer staples become more attractive as defensive plays

- Fixed income starts to compete seriously with equities for the first time in years

A global forecasting group now projects US full-year inflation at 4.2% -- significantly higher than the Fed's 2.7% estimate. If they are right, the single rate cut the market is pricing in may never arrive.

What Earnings Season Actually Tells Retail Investors

Earnings season officially kicks off with the big banks this week, and the pattern emerging is important. JPMorgan beat estimates. Citigroup and Wells Fargo report Monday April 14. Netflix reports April 16. Then comes the real test: tech.

Here is what most retail investors miss about earnings season: the stock price reaction is not about whether a company beat or missed estimates. It is about what the guidance says about the next quarter and the next year.

JPMorgan's stock surged 4.2% not just because of the record profits, but because the succession announcement removed years of uncertainty ("succession risk") from the stock. Marianne Lake will take over as CEO on January 1, 2027. Dimon stays as Executive Chairman through 2028. Investors got clarity -- and clarity is worth money in a volatile market.

For the upcoming reports, watch for three things:

Consumer spending resilience. Any company with direct exposure to the US consumer -- retailers, restaurants, airlines, credit card companies -- will signal whether the spending data JPMorgan reported is holding up or starting to crack. Delta Air Lines reported on April 8 and will be closely watched for travel demand signals.

Margin protection. Companies that can pass higher energy and input costs to customers (pricing power) will outperform. Companies that cannot -- especially lower-margin consumer staples and industrials -- will see earnings squeezed.

Guidance, not history. The Q1 numbers reflect January through March. What matters more is what management says about Q2 and the full year. Watch for phrases like "uncertain macro environment," "monitoring geopolitical developments," and "revising guidance" -- these are the signals that the confidence is fading.

The Recession Debate: Who Is Right?

Here is the most uncomfortable reality of April 2026: the economy is giving contradictory signals simultaneously, and some of the smartest people in finance are on opposite sides of the recession debate.

On the bearish side:

- Moody's Analytics: 49% recession probability within 12 months -- the highest since 2022

- Goldman Sachs: 30% recession odds, warning that sustained oil above $150 could push the S&P 500 to 5,400

- NerdWallet survey: 65% of consumers expect a recession within the next year

- S&P 500 Death Cross: The 50-day moving average crossed below the 200-day in late March -- historically a bearish signal

On the bullish side:

- JPMorgan's results: $16.4 billion net income, consumer spending up 2.6%, no signs of credit crisis

- Loomis Sayles: Projects 15% recession probability, expects double-digit S&P 500 earnings growth for 2026

- ETF inflows: $462 billion flowed into ETFs in Q1 2026 -- investors are still buying the dip

- Jobs: 281,000 jobs added in March, significantly beating estimates. Unemployment at 4.3%

The honest answer is that both sides are looking at real data. The economy is genuinely at a crossroads. The outcome depends heavily on a variable that no economist can model with precision: when does the Iran conflict resolve?

Pakistan's prime minister brokered a two-week deadline extension this week, buying time for negotiations. If the Strait of Hormuz fully reopens by early May, oil could quickly retrace to $75-80, inflation pressures ease, and the Fed could resume cutting rates in the second half of the year. Markets would likely rally sharply on that news.

If the conflict escalates or drags on past June, the stagflation scenario -- rising inflation combined with slowing growth -- becomes increasingly likely.

How Smart Investors Are Positioning Right Now

The right response to a market of contradictory signals is not to bet everything on one outcome. It is to build a portfolio that performs reasonably well across multiple scenarios. Here is how informed investors are thinking about positioning right now:

Financials for the "soft landing" bet. If JPMorgan's earnings resilience is a preview of what the rest of the banking sector will report, financial stocks remain attractive. Citigroup and Wells Fargo report next week. Strong results would confirm that the credit cycle is normalizing rather than cracking. The XLF (financial sector ETF) has outperformed the broader market year-to-date.

Energy for the "conflict continuation" hedge. Oil companies like ExxonMobil, Chevron, and smaller E&P names benefit directly from $100+ oil. If you believe the Iran conflict will drag on, energy is a straightforward hedge. The XLE (energy sector ETF) has been one of the best-performing sectors of 2026.

Gold as the volatility insurer. Gold is trading near $4,761, up from $3,200 a year ago. Analysts are targeting $5,000+ as a near-term level. In an environment of elevated inflation, geopolitical risk, and weakening dollar, gold has played its traditional role as a store of value. It belongs in most portfolios as a small-but-important allocation.

Fixed income as the new competitor to equities. With the 10-year Treasury yielding 4.33%, bonds are genuinely competing with stocks for the first time in years. For investors who cannot stomach volatility, short-to-medium term Treasuries offer attractive risk-free returns. The case for a 100% equity portfolio has weakened.

Selective tech, not blanket tech. The "Magnificent Seven" era of buying every tech stock indiscriminately is over. Microsoft is down 23% year-to-date. But Broadcom surged 6.2% this week after announcing long-term AI deals with Alphabet and Anthropic. The winners will be companies with real, monetizable AI revenue -- not just AI narratives.

The Week Ahead: What to Watch

The next seven days will provide significant new information for investors:

- April 11 (today): March CPI report -- the first to fully reflect war-related energy price impacts. Consensus expects 3.1-3.3% year-over-year. A number above 3.5% would likely trigger a bond selloff and push rate cut expectations even further out.

- April 14: JPMorgan's actual Q1 report release (already previewed), plus Citigroup and Wells Fargo. The focus will shift to guidance and what bank CEOs say about the second half of the year.

- April 16: Netflix reports. As a bellwether for consumer discretionary spending and streaming, their subscriber numbers will signal whether consumers are cutting back on entertainment.

- Iran/Strait of Hormuz: The two-week deadline extension runs out in late April. Any diplomatic progress -- or military escalation -- will be the most market-moving event of the month.

In a market where record-breaking profits coexist with near-50% recession odds, the temptation is to do nothing and wait for clarity. That is understandable. But historically, the investors who build positions during uncertainty are the ones who generate the best long-term returns.

Jamie Dimon has said repeatedly: "The United States of America's best days are ahead of us." He said it again this week, even as he warned about geopolitical risks. A man who just posted the most profitable quarter in Wall Street history, and who is voluntarily stepping down from one of the most powerful jobs in finance, still believes in the long-term arc of the market.

The question is not whether the market will recover. History says it will. The question is: will you be invested when it does?

What if you could be the first to uncover the latest trends, insights, and opportunities?

Dive into our community today and get a head start on the market!

Get exclusive access to cutting-edge updates, expert opinions, and must-know news -- all in one place.

STAY AHEAD OF THE GAME!

Let's Build Wealth & Give Wealth!

Together, Next Level